Equities hang in there, rates and bonds stable. US finally outperforms Europe YTD. Key week with US CPI, US PPI, the Fed and the ECB. The Fed should pause, hike 25bps in July, and then stop (inflation permitting). Continue to be positive on equities, even if the market does feel extended and prone to consolidation/correction and neutral on bonds.

Major market events 12th – 16th June 2023

Highlights for the week

Mon: JP PPI, IN CPI.

Tue: UK Unemployment Rate, DE CPI, US CPI.

Wed: UK Trade Balance, UK GDP, EU Industrial Production, US PPI, US Interest Rate Decision.

Thu: JP Exports, JP Trade Balance, CN Industrial Production, CN Unemployment Rate, CH PPI, FR CPI, EU Trade Balance, EU Interest Rate Decision, US Retail Sales, US Philly Fed Manufacturing Index, US Initial Jobless Claims, US Industrial Production, US Capacity Utilization.

Fri: EU CPI, US Michigan Consumer Sentiment.

Performance Review

- The market is due for consolidation after a great ride – it should catch its breath. Selling pressure does resurface every week, but when I start thinking ‘This is it (the start of the decline), the market surprises me once more with a bounce. The S&P 500 and the Dow Jones eked out small gains last week, while the Nasdaq 100 closed in negative territory. The US finally overtook Europe in terms of YTD performance. With 1Q23 now over, the focus will shift to 2Q23, starting with Oracle on Monday. The estimated earnings decline for 2Q23 is -6.4% (-4.8% on March 31st), which follows in synch the forecasts for 1Q23. What worries me is that these forecasts have been worsening in the last two months; we will soon see if they have in them what is needed to overturn this trend.

- Value and growth were even in a volatile week. The Nikkei 225 continues relentlessly on its march higher. It and the Nasdaq 100 are the two markets most likely of making a pullback but do not underestimate the power of liquidity. It is possible that there is ongoing an epochal change in how the Japanese savers manage their money. Even a small increase in equity weightings would mean a lot for the market. To be clear: while I would not buy Japan at these levels, I would not short it either. It’s probably best to stay on the sidelines, at least until the next BOJ meeting on July 27-28. If the economy continues to perform well, I think the JPY will continue to weaken (which in turn will be a positive for the economy) – look after your hedges!

- The S&P 500 managed to survive unscathed its third week after the breakout. This is a big week, with the Oracle results, CPI, PPI, and last but not least the Fed, which can tilt the market one way or the other. I’m happy to stay long with the S&P 500, using its previous Feb 2 peak – 4,179.76 – as a stop. Goldman Sachs has just raised its YE23 target for the S&P 500 to 4,500. On top of that they have just completed a study on the impact of AI on the market, productivity improvement, and valuation, and conclude that, on a market level at least, investor optimism for AI is not yet at extreme levels (though some of the stocks are). This, in turn, is positive for the Nasdaq as well – but watch out for a pullback. Europe is in a more tricky position: it needs a sustained performance of broader equities (not technology) to go higher, and the rates environment might be more complicated and farther from the top than the US – let’s see what the ECB will say this week. Should it manage to reach its previous high set in July 2007 (4524.45) and make a breakout above that level it would signal another leg up for equities.

- The Fed meets on Jun 13-14 and expectations for a rate hike have meaningfully changed since last week, with the CME FedWatch tool market pricing a 23.6% probability of another hike in June, but a 78.6% of another hike in July (which in all likelihood would be the last and would take the target value for the Fed Funds to 5.25% to 5.50%). There is growing consensus that the current level of rates is at a restrictive level for the economy, and therefore Governor Powell could continue to keep it at the same level for the rest of the year to further tame inflation, which he and other board members have acknowledged is still too high. Goldman Sachs is also forecasting a pause in June and a 25bps hike in July, After having gone past the rates tantrum, the baton passes on to the economy, which so far has performed admirably, despite the tough environment. In 2H23 it is expected that the economy will meet a more benign rate environment, although we need to see if earnings will indeed trough in 2Q23 and whether they will bounce in the back half of the year. It is important to see if bottom-up forecasts for both 2023 and 2024 continue to be cut or, at some point, manage to find their feet. It is also very important to check if the 7 leading companies (MAGMA – Microsoft, Apple, Google (Alphabet), Meta, and Amazon. plus Tesla and Nvidia) continue to perform in line with 1Q23 and if there is an expansion of breadth (which would be very important for the market) and a follow through to other companies.

- 1Q23 earnings reports are drawing to an end, with 99% of S&P 500 companies having reported. We will get the first glimpse of 2Q23 from Oracle on Monday, which will be closely watched.

Checking up on the economy: the good

The ‘good’ points to more sustained growth and no recession, albeit at the cost of higher rates (the ‘higher for longer’ moniker that is soon becoming a mantra), even though expectations for rate cuts are mounting in 2024. There does seem to be a change in the narrative though, at least according to what is being priced by the market, with rates becoming less of a concern and the economy’s performance becoming more of a concern. Introducing the Atlanta Fed GDPNow estimate for 2Q23, which at 2.2% would account for very solid growth, revised higher from 2.0% previously. As before, there is a meaningful difference between this forecast and the consensus for Blue Chips; at some point, they will have to converge. It is good and notable to see that these are in positive territory and that they have been improving (=no recession) in the last two months or so, with the Blue Chips consensus moving towards 1%.

Source: Blue Chip Economic Indicators and Blue Chip Financial Forecasts

As mentioned before, Goldman Sachs is introducing a new, YE 2023 forecast for the S&P 500 of 4,500. The investment bank has a higher than consensus top-down forecast on S&P 500’s earnings ($224 vs bottom up consensus $221.66. top-down consensus $206, J.P. Morgan $205, Bank of America $200, and Morgan Stanley $195). Moreover, they came out with a new piece on the influence of AI which sees productivity to improve in the future from current levels, and also benefit from a reduction of their forecasts of a recession.

Source: Goldman Sachs Global Investment Research

Goldman Sachs is one of the first houses to quantify the impact that AI could have on productivity, return and valuations, with a central scenario which sees an increase of 9% on the S&P 500’s fair value. What is really significant is the impact it could have on earnings over the next 20 years. It could me (and in my opinion it will!) a game changer much as it was the early arrival of internet in the late 90’s. Of course, the timing of this in uncertain, and investors should not get overexcited. Buying Cisco at 100x forward revenue in 2000 yielded very poor results. It makes NVIDIA’s current valuation pale in comparison!

Source: Goldman Sachs Global Investment Research

Source: Goldman Sachs Global Investment Research

Source: Goldman Sachs Global Investment Research

Finally Goldman Sachs has cut its recession forecast back to 25%. If you look at its scenario analysis, 60% points to a strong economy. In fact, they posit that going forward there will be more hikes, less risks. Their baseline scenario doesn’t see any cuts in 2023, and sees the terminal rate at 5.25-5.50% after the hike in July. Should inflation continue to surprise on the upside Fed Fund rates could well reach 6% over time; but Goldman Sachs expects inflation to decline in 2H23. Their view contemplates a stronger US GDP than consensus for all of 2023 and most of 2024.

Source: Bloomberg, Goldman Sachs Global Investment Research

Source: Goldman Sachs Global Investment Research

Source: Goldman Sachs

Checking up on the economy: the bad

Let’s start with this chart with a very useful reminder: earnings do not survive recessions. So we absolutely must avoid one if we are to thrive. The yield curve has been inverted for a while and it continues to get even more inverted and hence predictive of a recession. Nothwithstanding the economy’s strong run this continues to cast doubts about the future.

Source: J.P. Morgan

On top of that, the ISM Manufacturing Index is also in contraction, signalling a recession, although

the spread between high yields and investment grade in the US – another potential indicator of weakness – remain tight.

Source: BofA Global Investment Strategy, Bloomberg

Checking up on the economy: the ugly

Valuation certainly isn’t cheap. It is even less so considering such appealing yields, particularly on the short end. This has led some to speculate that the current P/E is unsustainable. The current forward P/E of 18.5 is higher than the 10-Year average of 17.3. Hence earnings are of paramount importance. It is true that the market is expensive, but it much depends on the outlook for earnings in 2H23. If the economy can continue to perform, it would seem feasible to see the market trading around such multiples, perhaps with a slight compression due to the better results reported.

The staggering performance of the Magnificent Seven (MAGMA + Nvidia and Tesla) was in part fuelled by the AI boom, as these are the companies most exposed to this trend. This has, in turn, inflated their market capitalization, and increased their weighting in the index to a level never seen before, not even at the peak of the dot.com boom, where it must me noted that 2/5 of the group belonged to different sectors other than technology.

Source: Bloomberg, BofA US Equity & Quant Strategy

The chart below tells a tale of two halves. The 10 companies with the largest market cap in the S&P 500 (Apple, Microsoft, Amazon, Alphabet, Tesla, Berkshire Hathaway, Meta, Johnson & Johnson, UnitedHealth, and Bank of America) command a size of the S&P 500 which is equal to those of the 426 companies with the lowest market capitalization. This is not healthy as it exposes the market to a company specific risk – if any of the Top 10 should falter, the market would suffer as a consequence. There is a hint of risk management in this: investing in the S&P 500 as it is now (and even more so in the Nasdaq 100) brings on more risks and more volatility than in the past.

Source: ISABELNET.com

Sentiment and what the market is telling us

The Fear and Greed Index eventually made it into Extreme Greed territory, is still in Greed territory, ending the week with a reading of 77, This is another reason which brings me to approach the next week with a bit more caution, even though in the case of a surprise on inflation/rates the market will continue to rally no matter how overbought it is and despite the extreme greed.

Source: CNN Business

The lagging AAII Sentiment Survey asked a different question this week, which brought the bulls out of hibernation. I share the constructive view on equities, despite any weakness that there might be near term.

Source: AAII Sentiment Survey

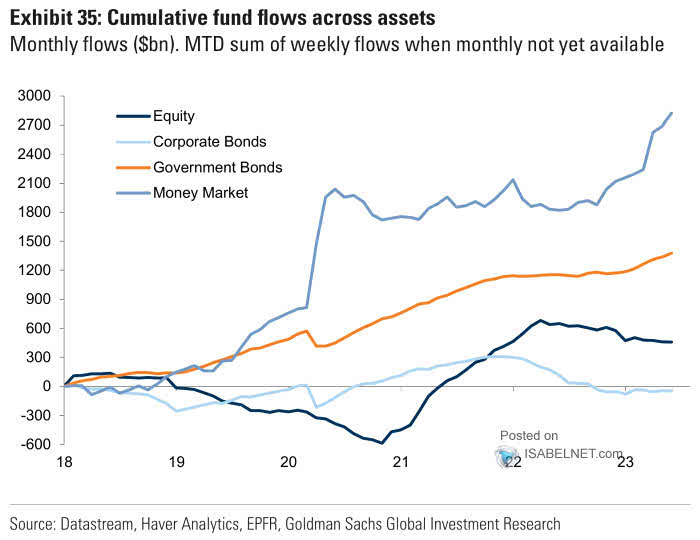

What are the Flows telling us?

Flows into equities might be turning, after abundant caution earlier in the year. Flows into Money Market funds remain as strong as ever, followed by Government Bonds, attracted by the high yields on offer.

Source: Datastream, Haver Analytics, EPFR, Goldman Sachs Global Investment Research

There was some profit taking in tech last week, which led to some outflows to capitalize the stellar performance so far. Still, the 4-week trend remains positive. Let’s see what happens next week.

Source: BofA Global Investment Strategy, EPFR

Earnings Review

Source: FactSet

The forward 12-month P/E ratio for the S&P 500 is 18.5x, up from last week’s reading of 18.0x, which is below the 5-year average at 18.6x but above the 10-year average at 17.3x. The present, bottom-up level ($222.61) is hovering around Goldman Sachs’ top-down $224 forecast, but it did manage to reverse its course after 1Q23. As we have been going down steadily for a while, I just wonder if at some point down the year the US Corporates will find in them what it takes to reverse this trend, as forecasted to happen in the back half of the year.

For 2Q23 the blended EPS decline for the S&P500 on aggregate is -6.4%. If correct, it will mark the third consecutive quarter in which there has been an earnings contraction, and it will represent the largest decline since 2Q20, when it was -31.6%. The upward revision to 2Q23 earnings growth (-6.4%), has been surprisingly negative if compared to 31 Mar’s -4.8%, but it is still early days. Despite the concern about a possible recession next year, analysts still forecast a positive growth in earnings for the overall market in CY 2023 of 1.2% year on year, vs 1.1% on Mar 31, while revenue is forecasted to grow by 2.4% vs 2.1% on Mar 31.

Source: FactSet

With estimates now measured against the forecasts as of Mar 31st, there are very few differences yet. Of note, Information Technology’s growth is now positive, and greatly outstripping both earlier negative forecasts (of as much as -1%) and their Mar 31st previous reference.

Source: FactSet

The S&P 500 has its revenue growth estimates at 2.4%, level with last week’s. Financials are still leading the pack in terms of revenue forecasts. Information Technology revenue growth has been revised upwards to 1.4% from as low as 0.7% and is now above to 1.3% on Mar 31st. The sector seems to be doing better on the top than on the bottom line, perhaps signaling the reason for some of the layoffs.

Source: FactSet

Let’s take a look at EPS for 2023 and 2024, which last week had the first upward revision in quite a while. The forecast for 2023 has now been updated to $221.66 from last week’s reading of $222.05; while 2024 is currently forecasted to be $247.31, compared to last week’s reading of $247.59.

Source: FactSet

This is the detail for 2Q23. While the market might be more concerned about rates and recession than earnings at this point, the narrative is changing from rate risk to macro risk where earnings will be of paramount importance. While the negative revisions to 2Q23 are a bit troublesome, I’m encouraged by the fact that on a yearly basis, there have been no more declines lately, which is remarkable considering the very limited breadth of the market. It is also well possible that earnings for 2Q23 too will surprise on the upside following a very positive 1Q23. Stay tuned.

Earnings, What’s Next?

The earnings season is now drawing to an end in its 1Q23 reports. In June we will have a first glimpse of 2Q23 (or at least the first two months of it) from companies, such as Oracle, that report a month early. Here’s a list of companies reporting this week. Highlights include Oracle (Monday, After Close), and Adobe (Thursday, After Close).

Source: Earnings Whispers

Market Considerations

Source: Bloomberg, BofA US Equity & Quant Strategy

Revenue growth estimates for 2024 are forecasted to grow by 4.9% (5.0% on Mar 31st) and earnings growth estimates for 2024 are predicted to grow by 12.3% (12.6% on Mar 31st), so the future looks to be bright. While we continue to debate whether the US economy will fall into a recession or not and what will be the peak rates for Fed Funds, and we welcome the arrival of a new bull market for the S&P 500 (+20% from the October lows), near term it is quite possible that we see a consolidation around current prices after such a big jump.

We are probably shifting from a monetary risk to a macro risk, where the performance of the economy is more important than what the Fed does. We should be mindful that the economy is probably just doing ok, even though passing the peak in rates will remove the overhang present on the market. If and when rates will diminish in importance, earnings (and top-line growth) will hopefully pick up their pace.

So the breakout happened, with both the S&P 500 and the Nasdaq 100 ahead of their previous Feb 2 highs. The strong performance of the Nikkei is a contributor to the global rally in equities. I tactically continue to suggest staying long on Equities, despite a possible consolidation/correction, as long as the S&P 500 Nasdaq 100 stay above their Feb 2 peaks. If those levels hold, it would open a new leg up for equities and for the market; if they don’t, we fall in double-top territory with the markets possibly revisiting their recent lows. Regarding bonds, the trajectory is that yields will eventually fall, albeit with a few bumps on the road.

For the less volatility prone of you, it may make sense to take all opportunities to alter the weights of your asset allocation by increasing the weights of safety assets at the expense of more risky assets by lightening up in equities and reinvesting in bonds at attractive (approx 4%) yields. For those willing to look besides US treasuries, investment grade bonds (LQD ETF) could also be a good compromise: 1.2% pickup over government bonds for the safest part of the credit complex may still be compelling. 10-Year yields were turbulent last week, both in the US and Europe, though the ceiling should be near for both. For those wishing to keep their money in Equities with lower volatility, suggest switching to Japan as the company with the most stable outlook (the country with the more precise picture of rates at the moment) until rate perspectives become clearer in the US and Europe. They got a boost given the recent buy recommendation by Warren Buffett, and the oracle is very rarely wrong. So Japanese Equities are now investable regardless of the lower volatility derived by being the only nation in G7 not to raise rates in the current environment. Just watch out for the JPY – if the current strength in the economy and markets is to continue, you may want to hedge it as it will likely continue to slide (against all major currencies).

Happy trading and see you next week!

InflectionPoint

Disclaimer

All views expressed on this site are my own and do not represent the opinions of any entity with which I have been, am now, or will be affiliated. I assume no responsibility for any errors or omissions in the content of this site and there is no guarantee for completeness or accuracy. The content is food for thought and it is not meant to be a solicitation to trade or invest. Readers should perform their investment analysis and research and/or seek the advice of a licensed professional with direct knowledge of the reader’s specific risk profile characteristics.

Leave a Reply